David vs Goliath

A call to staying small and nimble for longer

The fight over who wins in AI between OpenAI and Google is going to be a very interesting one. In this case, OpenAI is clearly David, whereas Google seems to have all the advantages. OpenAI has trawled the internet to build up a data set, whereas Google has done so for many years, created insights insights across music & video (YouTube), travel patterns (Maps), email, search, music, even the way we work with its GoogleDocs suite of product. AI is a commodity unless you have proprietary data and from a standing start its seems like an unfair fight.

Having said that, I think this is going to be a great test between what happens when a very focused company (OpenAI) battles a good company (Google) that is spread over different products and faces the innovators dilemma of disrupting its business internally before outsiders do.

We had a sample of this with the Slack versus Microsoft Teams competition. Let's be clear, Slack was by far the better product, but when you combine the fact that Teams gave you not just a productivity chat app, but a video conference alternative to Zoom, and then you layer on that with Microsoft's distribution, it seemed like it was a matter of time before Slack was crushed and so it came to be. Yet everyone knows that Slack was a much better product. Even to this day, when someone sends me a Team's invite, I actually try and log in about ten minutes earlier because it's so s***.

Banks vs neobanks

This David vs. Goliath battle is also relevant when I look at neobanks versus the banks. Historically, neo banks have performed best when they truly have a very clear competitive advantage over the banks. The example I like to give of is wise. Whereas they may not be seen as a bank, this is exactly what they offer whether it's a wallet function, debit card, foreign exchange, local and international payment - practically everything but loans. In a world where the majority of neobanks struggled to achieve sustainability, wise focused on getting its core product, foreign exchange, perfect before doing anything else.

They are the epitome of success for neo banks and this is because they have refused to dilute their offering by trying to do too many things at the same time. In a recent talk between Brian Chesky and Jason Calacanis on This Week in Startups, Chesky, who is the CEO of

“we have to have permission by the customer to do something new and we only have permission to do something new if they love what we currently do”

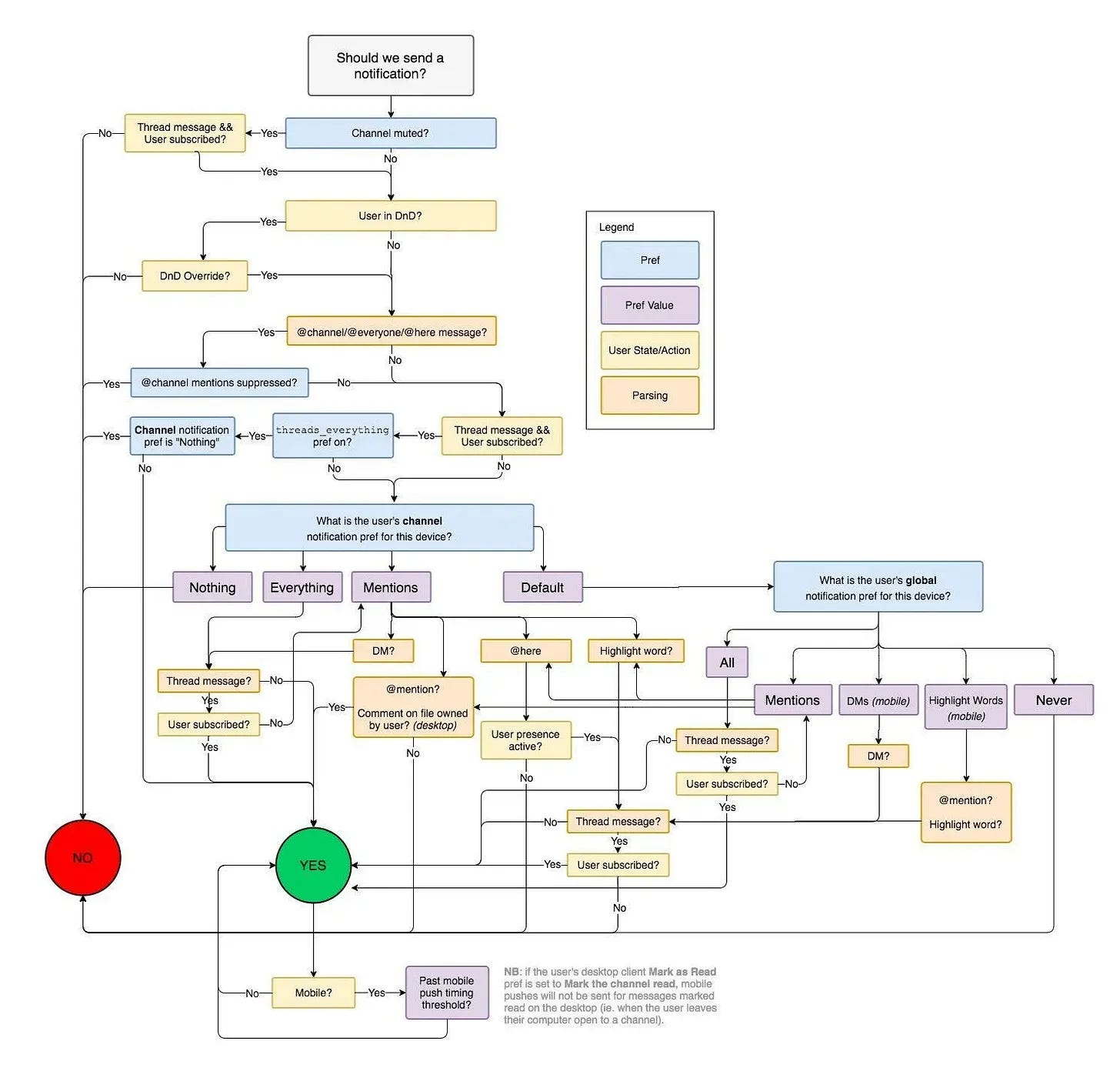

The argument being that if your your core product is s***, your customers are unlikely to go adopt any new extension. The reality is that when you add on a new product going from say one to two. You don't double the complexity of your operations, but you probably square it. The example I like to give is the chart below of what it takes in slack to send a notification. This is simply a notification. Just to be clear. Now imagine when you go from lending to transfers. It's f****** crazy.

I wish I had seen this video 5 years ago as we saw this firsthand at Carbon. Whilst we started off as a digital lender, our goal was always to be a Pan African digital bank. With the benefit of hindsight, we should not have launched our banking product yet until we really had lending shit hot.

The rationale we had at the time was yes that but to lend competitively we need a low cost of funds - we borrowed at 15-20% compared to the banks at 2-3% if they were being generous so there would always be and advantage they had over us. To get low cost of funds we need cheap deposits. To get cheap deposits we need bank accounts. To get bank accounts we then need to build new infrastructure.Then we get low cost of deposits.

What we failed to appreciate is the invisible costs of increased complexity of the system and trust building with the customer. When you are only lending money the customer doesn't have to trust you. All they care about is whether the borrowing rate is low enough and whether you will they give me enough money.

When you add a deposit product, the trust demands are is completely different. It's now will these guys keep my money? Can I trust them? Can I trust them at all times? It is this invisible cost that actually one should have factored in to say what, I can get customer deposits at 2% and corporate loans at 20%, but maybe that 18% spread is worth it because I have a simple business and I avoid all complications. Let me speak for neo banks and say that unless we really get it right, the customers will probably go for a teams like solution from their banks.

Founders beware

This is a mistake that I see many startups make.

Just like us at the time, founders are never going to listen because by default a founder is naive optimistic and believes that they can change the world.

Conventional wisdom says a product needs to be ten times better for customers to switch. I think this is why you're seeing inertia of customers worldwide resisting the allure of free banking, faster processing, free free free. The more the neobanks give away, the more customers stay with their tormentors legacy banks. We would be best served taking the route of wise and really perfecting our core product first - so we don’t become Slack.

It's not just in fintech the way you see the product extension of the core product offering. If I think locally, Reliance HMO started off as insurance but then has also become a healthcare provider. Moneypoint and Flutterwave have both moved into what starts resembling core banking services. There will very good arguments for the strategic shifts but my contention though is that as founders we need to be bold enough and brave enough sometimes to really get things right first, get the core product right first and then earn the permission of the customer to move forward.

That way many startups that begin like David - nimble, agile, focused - maintain their core strengths even as they scale and expand. This is something that I believe is not just good for eventual outcomes, but great for customers

This is a powerful post. Food for thought indeed.

But completely agree with narrowing focus and being nimble. That is all David has against Goliath.

Great points. I totally agree. Especially about Microsoft Teams being shit. :)